Stay Charged Up

Get the latest EV news, reviews, and analysis delivered to your inbox every week.

Get the latest EV news, reviews, and analysis delivered to your inbox every week.

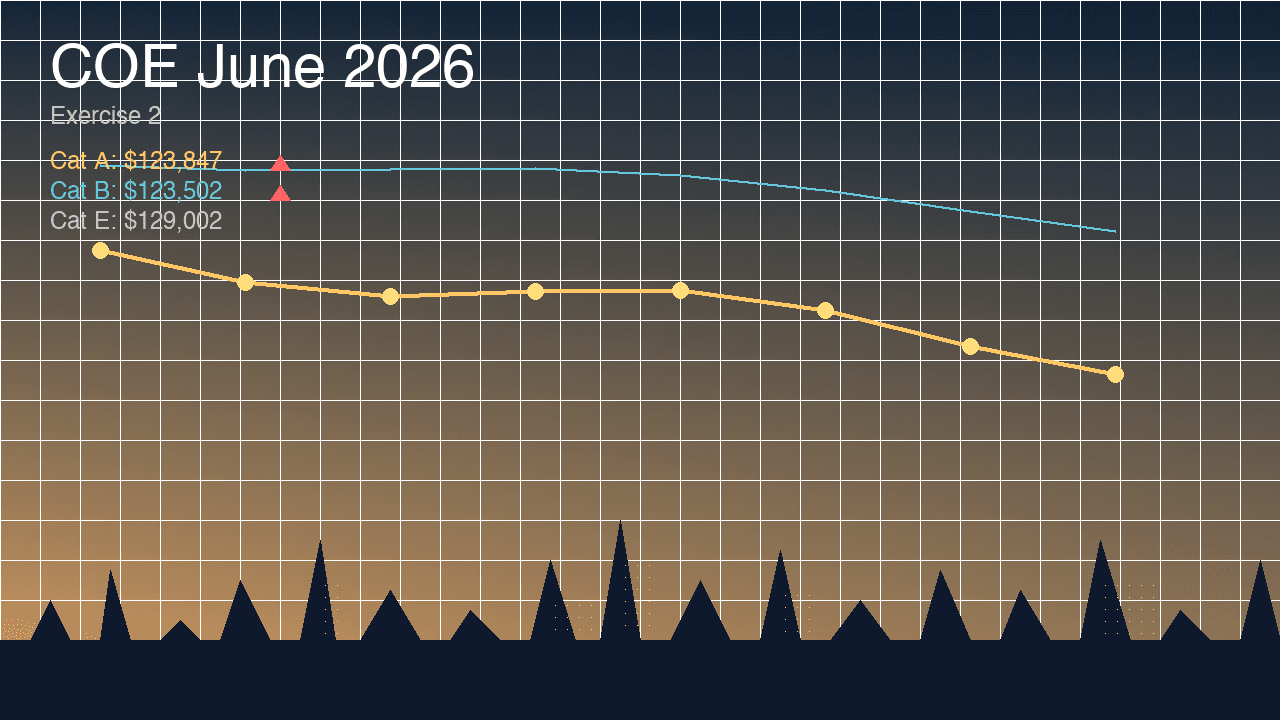

Cat A COE exceeded Cat B for the third time in four months, though both premiums fell from the previous exercise.

Sarah Chen

Certificate of Entitlement premiums for cars fell across the board in the second exercise of June 2026, but the headline remains a now-familiar anomaly: Category A closed at $123,847, once again surpassing Category B's $123,502. It is the third time in four months that smaller-engined cars have commanded a higher COE premium than their larger counterparts.

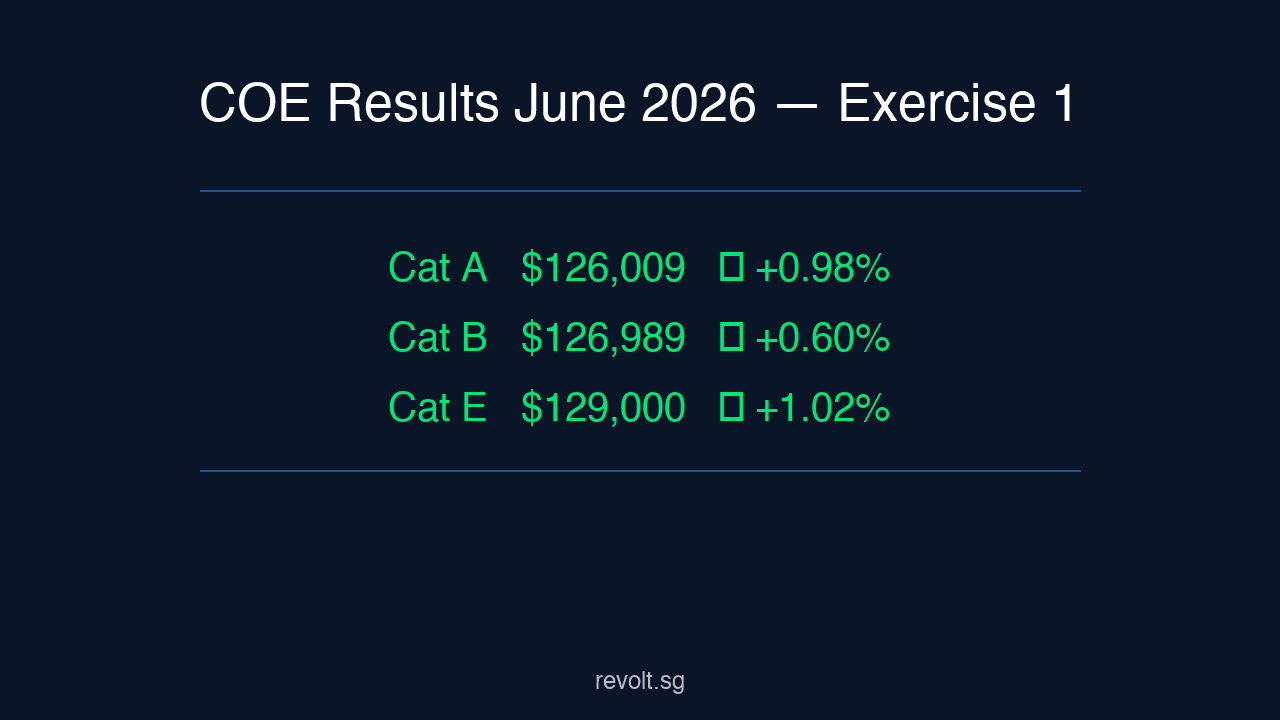

Cat A dropped $2,162 from the first June exercise, while Cat B saw a steeper decline of $3,487 — breaking a run of three consecutive exercises of rising premiums. The Open category (Cat E) settled at $129,002.

The Cat A–Cat B inversion has gone from curiosity to recurring feature. Since February 2026, three of the past eight exercises have closed with Cat A above Cat B, driven by two structural forces: the PARF rebate reductions that took effect earlier this year, and sustained demand for electric vehicles that fall within the Cat A power threshold of 110 kW or below.

What is notable about this latest inversion is how narrow it has become. The $345 gap between Cat A and Cat B is the smallest of the three inversions, suggesting the two categories are converging rather than one running away from the other. For EV buyers weighing a Cat A model against a Cat B alternative, the COE cost difference is now essentially negligible.

The Cat A bracket has become the landing zone for a growing cohort of battery electric vehicles. Models such as the BYD Dolphin, MG4 Standard Range, and several upcoming compact EVs from Chinese manufacturers all sit at or below the 110 kW ceiling. As more affordable EVs enter this segment, they compete for the same limited pool of Cat A certificates alongside traditional petrol hatchbacks and sedans — pushing premiums higher even as overall demand cools.

The PARF rebate adjustments have compounded this effect. With lower rebates available on deregistered vehicles, fewer existing car owners are cycling out of the system, tightening supply in a category where new EV entrants keep arriving. Cat B, by contrast, has a broader quota and faces less concentrated pressure from any single vehicle type.

Despite the inversion, there are signs of a cooling market. Oversubscription ratios eased across all categories in this exercise, indicating that fewer bidders are chasing each available certificate. The across-the-board decline in premiums — Cat A, Cat B, and Cat E all fell — reinforces the picture of a market taking a breath after several months of upward pressure.

For prospective buyers, the practical takeaway is straightforward. A Cat A EV and a Cat B EV now carry virtually the same COE burden. The decision between, say, a smaller LFP-battery compact and a larger NMC-powered sedan increasingly comes down to the vehicle itself — range requirements, charging habits, and intended use — rather than a meaningful difference in certificate cost.

Whether the Cat A–Cat B convergence holds will depend on the July quota announcements and the continued pace of new EV model launches in the sub-110 kW segment. Several manufacturers have confirmed Singapore launches in the third quarter that would add further Cat A-eligible models to an already crowded field. If supply remains tight and EV demand stays firm, the inversion may become less an anomaly and more a structural feature of Singapore's COE system.